Robertson's Tax & Accounting Services Limited

01764 456818

Registered Office : The Attic Studios, 23 High Street, Dunblane, Stirling FK15 0EE

|

You made it and filed your self-assessment return for 2018/19 by the 31 January 2020. However, having felt pleased with yourself, you realise to your horror that you have made a mistake and need to correct your return.

Can you do this and if so, how and by when? Yes, you can If you have made a mistake on your return, for example entered a number incorrectly or forgotten to include something, all is not lost. As long as you are within the time limit, the error can be corrected by filing an amended return. How? If you are in time to file an amended return, the process that you need to follow will depend on whether you filed your return online or on paper. Online returns If you filed your return online, you simply amend your return online. To do this:

Remember to check that it has been submitted and that you have received a submission receipt. Check the revised tax calculation too in case you need to pay more tax as a result of the changes, but remember to take account of what you have already paid. Paper return If you opted to file your return on paper by 31 October 2019, to make a change you will need to download a new tax return. This can be done from the Gov.uk website. Fill in the pages that you wish to change and write ‘Amendment’ on each page. Make sure you include your name and unique taxpayer reference (UTR) on each page too. Send the corrected pages to the address to which you sent your original return. Commercial software If you used commercial software to file the return, contact your software provider to find out how to file an amended return. If your software does not allow for this, contact HMRC. When You have until 31 January 2021 to make changes to your 2018/19 tax return. If you have missed the deadline, you will need to write to HMRC instead. This may be the case if you find a mistake in your 2017/18 return after 31 January 2020. In the letter, you will need to say which tax year you are amending, why you think you have paid too much or too little tax and by how much. You have four years from the end of the tax year to claim a refund if you have overpaid. Changes to the tax bill If amending the return changes the amount that you owe, you should pay any excess straight away. Interest will be charged on tax paid late. If your 2018/19 liability changes, your payments on account for 2019/20 may change too. If as a result of the changes made to the return you have paid too much tax, you can request a repayment from your personal tax account. Partner note: See www.gov.uk/self-assessment-tax-returns/correction. 19/2/2020

Incidental overnight expensesA tax exemption enables an employer to meet small personal expenses when an employee stays away from home for work, without the employee suffering a tax charge and without any need to report the expenses to HMRC.

What are incidental overnight expenses? Incidental overnight expenses are personal (i.e. non-business) expenses incurred when an employee travels overnight for business. Examples include:

How much is the exempt amount? The exempt amount is £5 per night for trips in the UK and £10 per night for overseas trips. These limits have not been increased. It should be noted that the exemption only applies if the expenses do not breach the limit. If amounts paid to the employee are more than the exempt amount, the full amount is taxable not just the excess over the exempt amount. Per trip not per day The exemption can be applied per trip rather than a day-by-day basis. This means that it will apply as long as the incidental overnight expenses paid for the trip do not exceed the allowance for the full trip – it does not matter if on a particular day the allowance is exceeded as long as on average within the exempt limit. The application of the allowance is illustrated by the following example. Example Rachel and Anna are colleagues and often travel on business. In January 2020, Rachel spent five consecutive nights away from home on a business trip in the UK. During the trip she incurred incidental expenses of £21 which were reimbursed by her employer. On one day, her expenses (for laundry) were £8. On the remaining four days, they were less than £5 per day. The exempt amount is £5 per day for overnight stays in the UK – equivalent to £25 for a five-night trip. As the expenses paid by her employer are less than £25, the exemption applies. It does not matter that on one day the actual expenses were more than the £5 daily limit. Anna also took a business trip during January, spending three consecutive nights in Germany. She incurred incidental expenses of £31 which her employer reimburses. For trips abroad, the exempt amount is £10 per night – a total of £30 for a three-night trip. As the amount paid by Anna’s employer is more than £30, the full amount is taxable and liable to Class 1 National Insurance. Partner note: ITEPA 2003, s. 240, 241. Pension savings can be tax efficient as contributions to registered pension schemes, attracting tax relief up to certain limits.

Limit on tax relief Tax relief is available on private pension contributions to the greater of 100% of earnings and £3,600. This is subject to the annual allowance cap. Tax relief may be given automatically where your employer deducts the contributions from your gross pay (a ‘net pay scheme’). Alternatively, if you pay into a personal pension yourself or your employer pays contributions into the scheme after deducting tax, the pension scheme will claim basic rate relief (‘relief at source’). Thus if you pay £2,880 into a pension scheme, your scheme provider will claim basic rate relief of £720, meaning your gross contribution is £3,600. If you are a higher or additional rate taxpayer, the difference between the basic rate tax and your marginal rate can be reclaimed from HMRC via your self-assessment return. Annual allowance The pension annual allowance caps tax-relieved pension savings – contributions can be made to a registered pension scheme in excess of the available annual allowance, but they will not attract tax relief. The annual allowance is set at £40,000 for 2019/20; although this may be reduced if you have high earnings. The annual allowance taper applies where both your threshold income is more than £110,000 (broadly income excluding pension contributions) and your adjusted net income (broadly income including pension contributions) is more than £150,000. Where the taper applies, the annual allowance is reduced by £1 for every £2 by which adjusted net income exceeds £150,000 until the annual allowance reaches £10,000. This is the minimum amount of the annual allowance. Only the minimum allowance is available where adjusted net income is £210,000 or more and threshold income is more than £110,000. The annual allowance can be carried forward for up to three tax years if it is not used, after which it is lost. The current year’s allowance must be used first, then brought forward allowances from an earlier year before a later year. Example Harry has income of £100,000 in 2019/20. He has received an inheritance and wishes to make pension contributions of £60,000. In the previous three years he has used £10,000 of his annual allowance, leaving £30,000 to be carried forward for up to three years. To make a contribution of £60,000 for 2019/20, Harry will use his annual allowance of £40,000 for 2019/20 and £20,000 of the £30,000 carried forward from 2016/17. The £10,000 remaining of the 2016/17 allowance will be lost as cannot be carried forward beyond 2019/20. The unused allowances of £30,000 for 2017/18 and 2018/19 can be carried forward to 2020/21. Reduced money purchase annual allowance A lower annual allowance of £4,000 (money purchase annual allowance (MPAA)) applies to those who have flexibly accessed pension contributions on reaching age 55. This is to prevent recycling of contributions to secure additional tax relief. Lifetime allowance The lifetime allowance places a ceiling on your pension pot. For 2019/20 it is set at £1,055,000. A tax charge will apply if you exceed the lifetime allowance. Partner note: FA 1994, s. 227ZA, 288, 228ZA, 218. The trivial benefits exemption allows employers to provide employees with low cost benefits free of tax and National Insurance and any reporting obligations. For the purposes of the exemption, a benefit is trivial if the cost per head is not more than £50. Where trivial benefits are provided to an officer of a close company or a member of their family or household, an annual cap of £300 per tax year also applies.

For the exemption to be available, the benefit must not be provided in return for services provided and the employee must not be contractually entitled to receive the benefit. Contractual entitlement Contractual entitlement is wider than simply inclusion in the contract of employment. Consequently, the fact that the contract makes no reference to the provision of trivial benefits is not enough to satisfy the conditions for the exemption. In the December 2019 issue of their Employer Bulletin, HMRC highlighted a number of ways in which a contractual obligation may arise, including:

If any of these provide for the employee to receive the trivial benefit, the exemption will not apply. Beware of creating a ‘legitimate obligation’ Employers seeking to make use of the trivial benefits exemption should also be wary of falling into the ‘legitimate expectation’ trap; a contractual obligation may also arise is the employee has a legitimate expectation to receive the benefit. In the December 2019 issue of Employer Bulletin, HMRC illustrate this with an example of an employer who provides employees with a cream cake each Friday. While there is no contractual obligation for the employer to provide the employees with a cream cake on a Friday, the fact that the employer does so every Friday creates a legitimate expectation, taking the provision of the cakes outside the trivial benefits exemption. Frequency seems to be a problem here – HMRC seemingly do not apply the legitimate expectation argument where a benefit is provided annually, even if it is provided each year. HMRC’s Employment Income Manual at EIM21867, states: “Just because a gift is provided each year, or is provided to all staff members, does not mean that the employee has a contractual entitlement to it.” The guidance instructs HMRC officers that they “should not normally challenge modest gifts that are provided infrequently to employees, just because they are given to employees each year – for example, a Christmas or birthday gift”. Good practice To avoid falling into the legitimate expectation trap, vary both the nature and timing of trivial benefits provided to employees. Partner note: ITEPA 2003, s. 323A. From 6 April 2020, new appropriate percentage bands – and new lower charges for low emissions cars – will apply for company car tax purposes. From the same date, the way in which carbon dioxide emissions are measured is also changing. This means that in order to find the correct appropriate percentage for working out the taxable benefit of a company car, you will need to know whether the car was registered on or after 6 April 2020 or before that date, as well as the level of the car’s CO2 emissions. As a transitional measure, with the exception of zero emission cars, the appropriate percentage for cars registered on or after 6 April 2020 is 2 percentage points lower than cars registered prior to that date for 2020/21 and one percentage point lower for 2021/22. The figures are aligned from 2022/23. For zero emission cars, the charge is 0% for 2020/21, 1% for 2021/22 and 2% from 2022/23, regardless of the date on which the car is registered. The maximum charge is capped at 37%, and the diesel supplement applies as now. More information will be needed to work out the appropriate percentage where the car’s CO2 emissions (however measured) fall in the 1—50g/km band. From 6 April 2020, this band is sub-divided into five further bands, each with their own appropriate percentage. The band into which the car falls depends on its electric range (also known as its zero emission mileage). This is the maximum distance that the car can be driven in electric mode without having to recharge the battery. The relevant bands are as follows:

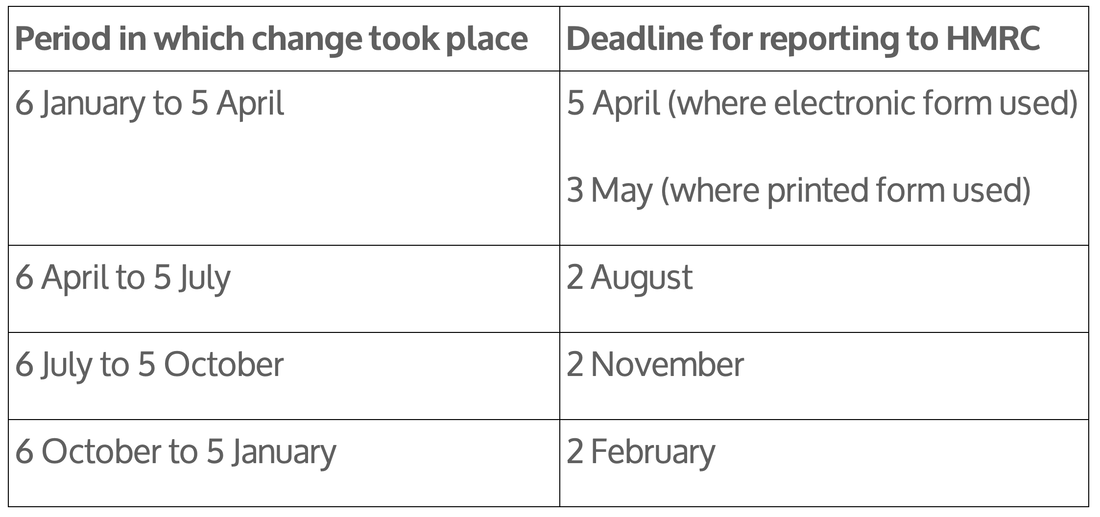

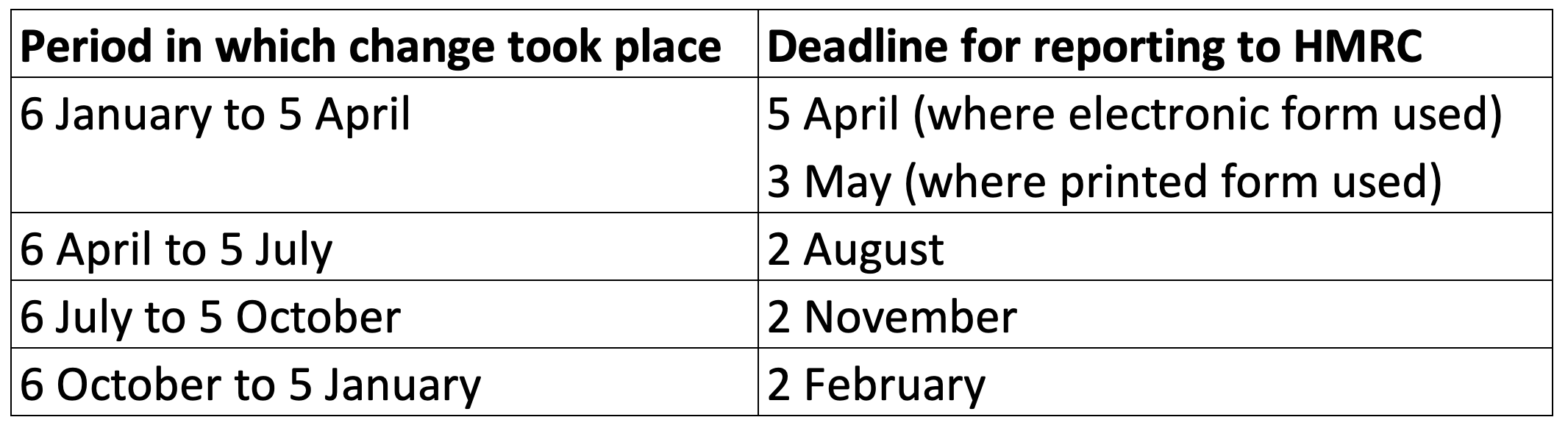

The greater the car’s zero emission mileage, the lower the appropriate percentage. Splitting the 1—50g/km band introduces additional reporting requirements. The precise nature of those changes depends on whether car and fuel benefits are payrolled. Payrolled benefits Where car and fuel benefits are payrolled, information on cars provided to employees is submitted to HMRC on the Full Payment Submission (FPS), rather than on form P46(Car). From 6 April 2020, where an employee has a car with carbon dioxide emissions that fall within the 1—50g/km band, the car’s zero emission mileage must be reported to HMRC in the new field that will be available from that date. P46(Car) changes If car and fuel benefits are not payrolled, form P46(Car) provides the mechanism for letting HMRC know when an employee has been given a car for the first time or given an additional car. The form can be submitted in various ways – on paper, using the online service or PAYE online. From 6 April 2020, the form will have an additional field for zero emission mileage which must be completed when providing an employee with a car with CO2 emissions in the 1—50g/km band. The deadlines for submitting the form are unchanged and are as shown in the table below.  Partner note: Income Tax (Pay As You Earn) Regulations 2003 (SI 2003/2682), regs. 61E, 61F, 90; HMRC Employer Bulletin December 2019.

From 6 April 2020, new appropriate percentage bands – and new lower charges for low emissions cars – will apply for company car tax purposes. From the same date, the way in which carbon dioxide emissions are measured is also changing. This means that in order to find the correct appropriate percentage for working out the taxable benefit of a company car, you will need to know whether the car was registered on or after 6 April 2020 or before that date, as well as the level of the car’s CO2 emissions. As a transitional measure, with the exception of zero emission cars, the appropriate percentage for cars registered on or after 6 April 2020 is 2 percentage points lower than cars registered prior to that date for 2020/21 and one percentage point lower for 2021/22. The figures are aligned from 2022/23. For zero emission cars, the charge is 0% for 2020/21, 1% for 2021/22 and 2% from 2022/23, regardless of the date on which the car is registered. The maximum charge is capped at 37%, and the diesel supplement applies as now. More information will be needed to work out the appropriate percentage where the car’s CO2 emissions (however measured) fall in the 1—50g/km band. From 6 April 2020, this band is sub-divided into five further bands, each with their own appropriate percentage. The band into which the car falls depends on its electric range (also known as its zero emission mileage). This is the maximum distance that the car can be driven in electric mode without having to recharge the battery. The relevant bands are as follows:

The greater the car’s zero emission mileage, the lower the appropriate percentage. Splitting the 1—50g/km band introduces additional reporting requirements. The precise nature of those changes depends on whether car and fuel benefits are payrolled. Payrolled benefits Where car and fuel benefits are payrolled, information on cars provided to employees is submitted to HMRC on the Full Payment Submission (FPS), rather than on form P46(Car). From 6 April 2020, where an employee has a car with carbon dioxide emissions that fall within the 1—50g/km band, the car’s zero emission mileage must be reported to HMRC in the new field that will be available from that date. P46(Car) changes If car and fuel benefits are not payrolled, form P46(Car) provides the mechanism for letting HMRC know when an employee has been given a car for the first time or given an additional car. The form can be submitted in various ways – on paper, using the online service or PAYE online. From 6 April 2020, the form will have an additional field for zero emission mileage which must be completed when providing an employee with a car with CO2 emissions in the 1—50g/km band. The deadlines for submitting the form are unchanged and are as shown in the table below.  Partner note: Income Tax (Pay As You Earn) Regulations 2003 (SI 2003/2682), regs. 61E, 61F, 90; HMRC Employer Bulletin December 2019.

The high-income child benefit charge (HICBC) applies to claw back child benefit from either the claimant or his or her partner where at least one of them has income of £50,000 or more. The charge is perhaps one of the more unfair tax charges in that the person who suffers the liability may not be – and often isn’t – the person who received the child benefit.

Nature of the charge The charge may apply to an individual with income over £50,000 where either they or their partner has received child benefit in the tax year. It may also bite where someone else gets child benefit for a child who lives with you and they contributed an equal amount to the child’s upkeep. It does not matter whether the child living with the individual is theirs or not. It is important to note here that ‘partner’ does not have to be a spouse or civil partner – the charge also applies to unmarried couples living together as spouses or civil partners. The measure of income for the purposes of the charge is ‘adjusted net income’. Broadly, this is income after taking account of Gift Aid donations and pension contributions and, for the self-employed, trading losses. Where both partners each have income in excess of £50,000, the charge is levied on the higher earner; if their income is the same, it is the person who receives the child benefit who pays the charge. How the charge is calculated The charge claws back 1% of child benefit for every £100 by which adjusted net income exceeds £50,000. Where adjusted net income is £60,000 or more, the charge is 100% of the child benefit received in the tax year. Example 1 Suki claims child benefit for her two children. This is set at £20.70 per week for the eldest child and at £13.70 for her youngest child – equal to £1,788.80 for 2019/20. Suki earns £30,000 from her job as a teacher and her husband Yuto earns £55,000 (after pension contributions) from his job in IT. As Yuto’s adjusted net income is more than £50,000, the HICBC bites. It is equal to 50% ((£55,000 - £50,000)/100 x 1%) of the child benefit received by Suki in the year, i.e. £894.40. Example 2 Matthew and Maria have two children in respect of which Maria claims child benefit, equal to £1,788.80 for 2019/20. Matthew has adjusted net income of £58,000 and Maria has adjusted net income of £72,000. As the higher earner, Maria is liable for the HICBC. As her adjusted net income is more than £60,000, the charge is equal to the child benefit paid in the year, i.e. £1,788.80 Paying the charge Where a person is liable for the HICBC, they must declare it on their self-assessment tax return. The tax can be paid via self-assessment. Alternatively, if the tax return was filed by 30 December 2019 and the underpayment for the year in total is less than £3,000 it can be collected through PAYE via an adjustment to the tax code. Worth stopping the claim? Where the charge is equal to the full amount of the child benefit, it may seem easier not to claim it, rather than claiming it only to have to pay it back. However, child benefit paid for a child under 12 comes with National Insurance credits, helping to build up entitlement to the state pension. If the claimant does not otherwise pay sufficient National Insurance for the year to be a qualifying year, failing to claim may adversely affect their state pension. The solution is to claim but elect not to receive the benefit. Partner note: ITEPA 2003, ss. 681B – 681H. There are a number of tax concessions available to married couples and civil partners which recognise that their financial affairs may be interlinked. One of these concessions relates the transfer of assets between spouse and civil partner for capital gains tax purposes. The disposal is deemed to take place at a value which gives rise to neither a gain nor a loss. This means that the spouse or civil partner making the disposal does not end up with a capital gains tax bill; the spouse or civil partner acquiring the asset simply takes over his or her partner’s base cost. This rule can be very useful from a tax planning perspective as the following case studies show.

Case study 1 Jane and John have been married for a number of years. Jane has built up a portfolio of shares, which she wishes to now sell so that the couple can take a mid-life gap year. The sale of the shares will realise a gain of £30,000. Jane is a higher rate taxpayer and John is a basic rate taxpayer. Neither has used their 2019/20 annual exemption and the intention is to sell the shares before the end of the 2019/20 tax year. The annual exemption for 2019/20 is set at £12,000. If Jane simply goes ahead and sells the shares, she will realise a chargeable gain of £18,000 after deducting the annual exempt amount. As a higher rate taxpayer, the gain will be taxed at 20%, giving rise to a capital gains tax bill of £3,600. However, if Jane and John make use of the inter-spouse exemption to transfer shares which would otherwise give rise of a gain of £18,000 to John, the position is very different. Jane is left with a gain of £12,000 which is covered by her annual exempt amount, leaving nothing in charge. John, however, is left with a chargeable gain of £6,000 (£18,000 - £6,000) after deducting his annual exempt amount. As the gain falls within his basic rate band, it is taxed at 10%, resulting is a capital gains tax liability of £600. By making use of the inter-spouse exemption, the couple’s combined capital gains tax bill is reduced by £3,000. Case study 2 Karamo owns an investment property jointly with his civil partner Robert. The property is let and the couple receive rental income of £20,000 a year. Karamo is a higher rate taxpayer, whereas Robert is in the process of setting up a photography business and earning around £14,000 a year. Each civil partner is deemed to have received rental income of £10,000 a year. Karamo pays tax of £4,000 (£10,000 @ 40%) on his share, while Robert pays tax of £2,000 (£10,000 @ 20%) on his share. The total tax paid on the rental income is therefore £6,000. By making use of the inter-spouse exemption, Karamo transfers his share of the property to Robert. As a result, Robert receives all the rental income, which is now all taxed at 20%, reducing the tax bill to £4,000, saving the couple £2,000 a year. Partner note: TCGA 1992, s. 58. 21/1/2020

Correcting an overpayment of wagesMistakes happen, and it can be very easy inadvertently to pay an employee too much when doing the wages. Perhaps a number was keyed in incorrectly or figures were transposed, or maybe commission was overstated or an employee was paid for more overtime hours than they actually worked.

From an employment law perspective, an employer has the right to recover overpayments of wages from the employee. But what needs to be done to correct the mistake for tax and National Insurance purposes? Adjustments during the tax year It is relatively straightforward to correct an overpayment of wages where the mistake is discovered in the same tax year and the employee continues to be employed. You will need to agree with the employee how the money is to be recovered. You may simply deduct it from future pay, or alternatively the employee may refund the overpayment to you. Where the overpayment is deducted from future pay, the correct approach is to deduct the net overpayment from net pay (i.e. after tax and National Insurance have been deducted). The mistake should be corrected in the next Full Payment Submission (FPS) sent to HMRC – this should show the correct payments to date and the correct net tax to date. The effect of this is that the PAYE deducted from the overpayment can be set off by reducing the next monthly remittance sent to HMRC. The employer should keep a note of both the reason for the adjustment and the method used to recover the net pay from the employer. Mistakes discovered after the end of the tax year If the mistake is not discovered until after the end of the tax year, it will be necessary to submit an FPS showing the correct year to date figures as at 5 April at the end of the tax year in which the mistake occurred. For 2018/19 and earlier tax years, mistakes discovered after the end of the year can also be corrected using an Earlier Year Update (EYU); however, HMRC will not accepts EYUs for correcting 2019/20 mistakes post year-end. The employee should also be informed of the mistake and given a replacement P60, clearly marked ‘replacement’. The employer will also need to agree with the employee how the overpayment is to be recovered. Partner note: Employer Further Guide to PAYE and NIC (CWG2) 2019—20, para. 1.19. As a general rule, travel between home and work is regarded as private travel and if the employer meets the cost of that travel, a benefit-in-kind tax charge will be triggered. However, it is possible for employees with a company van to use that van to travel between home and work, and for the employer to meet the cost of fuel for such journeys, without a tax charge arising. However, as with most tax exemptions, there are stringent conditions to be met.

Tax charge on company vans Where an employee has the use of a company van and private use of that van is unrestricted, a tax charge arises. The amount charged to tax is £3,420 for 2019/20. This gives rise to a tax bill of £684 for a basic rate taxpayer, £1,368 for a higher rate taxpayer and £1,539 for an additional rate taxpayer. Where fuel is also provided, a separate fuel charge applies; the taxable amount is set at £655 for 2019/20. No charge arises if the van is used only for business journeys or in respect of vans that meet the conditions to be regarded as a pool van. Restricted private use It is also possible to escape a tax charge but to be able to use the van for home to work travel if a condition – known as the ‘restricted private use condition’ – is met. This comprises two parts:

The second requirement is the business travel requirement. This is met if the van is available to the employee mainly for use for the purposes of the employee’s business travel. That is to say, the main reason that the employee has the van is because they need it for their job. The business travel requirement must be met at all times when the van is available to the employee. If the provision of the van is exempt, no fuel benefit arises, even if the employer meets the cost of home to work travel. Example Tony is a delivery driver. He is provided with a van by his employer for use in his work. He is allowed to take the van home at night and use it to drive to and from work. However, all other private use is prohibited. His employer pays for all fuel, including that for his journey between home and work. As the restricted private use condition is met, there is no tax to pay on either the provision of the van or the fuel. Partner note: ITEPA 2003, s. 155. |

IntroSnippets of news and interesting facts from the financial world Archives

February 2020

Categories |

RSS Feed

RSS Feed

28/2/2020